Salary vs. Dividend: Which Is Better for Ontario Small Business Owners in 2026?

If you run a corporation in Ontario, one of the most important financial decisions you face every year is how to pay yourself. Do you take a salary, pay yourself dividends, or use some combination of both? The answer isn’t one-size-fits-all — and getting it wrong can cost you thousands of dollars in unnecessary taxes.

The Case for Paying Yourself a Salary

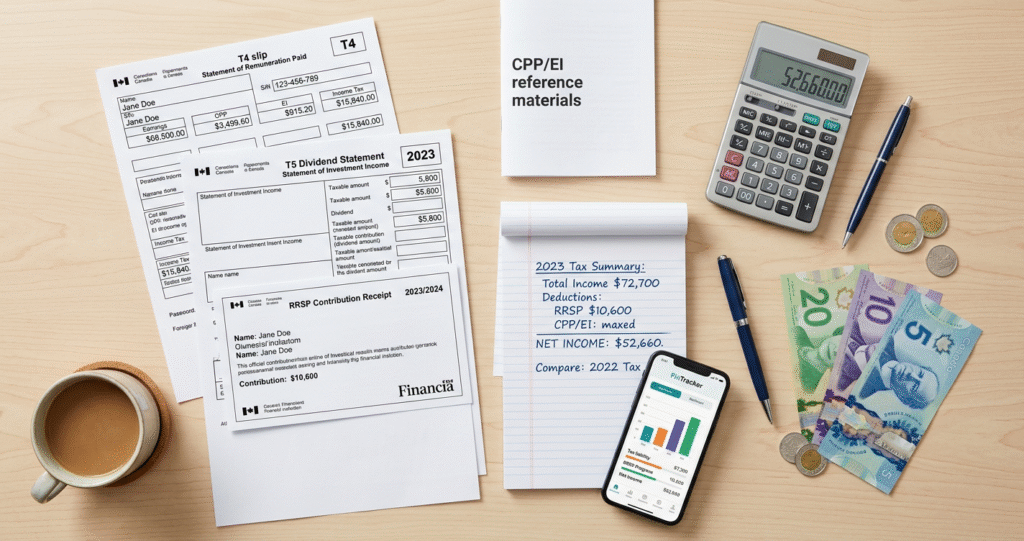

Taking a salary from your corporation means you’re treated like an employee. The corporation issues you a T4, deducts CPP contributions, and remits payroll to CRA. It’s familiar, predictable, and comes with some real advantages.

First, a salary is a deductible business expense, which lowers your corporation’s taxable income. That matters when your corporate profits are creeping above the small business deduction limit. Second, earned income creates RRSP contribution room. If building your retirement nest egg through an RRSP is part of your plan, you need employment or self-employment income to do it. Third, CPP contributions — while they feel like a cost today — translate into a pension benefit down the road. For some business owners, that guaranteed income in retirement is worth it.

The downside? Salary triggers both the employee and employer sides of CPP, and EI premiums may apply depending on your situation. Your personal marginal tax rate in Ontario can also climb quickly, especially once provincial and federal taxes stack up.

The Case for Paying Yourself Dividends

Dividends flow from your corporation’s after-tax profits. Because the corporation already paid tax on that money, the dividend tax credit gives you a break at the personal level to avoid double taxation. The result is often a lower effective tax rate compared to salary — particularly for eligible dividends paid from a Canadian-Controlled Private Corporation (CCPC) that has paid tax at the general corporate rate.

There’s no CPP on dividends, which means lower immediate costs. There’s also no EI deduction, and the paperwork is simpler — no payroll remittances, no T4 filings. For business owners who have other income sources or don’t need CPP, this can make dividends look very attractive.

The catch? No RRSP room is generated. If your retirement strategy leans heavily on your RRSP or spousal RRSP, a dividend-only approach can quietly undermine that plan. Dividends also don’t count as earned income for child care expense deductions, which matters for many Ontario families.

What About a Combination Approach?

Most experienced accountants — and for good reason — will suggest a blended strategy. A modest salary can generate just enough RRSP room and CPP contributions to meet your long-term goals, while dividends top up your personal income at a lower tax cost. The optimal mix depends on your total corporate income, your personal income needs, your family situation, and how close you are to the small business deduction threshold of $500,000 in active business income.

The 2026 tax year brings no dramatic changes to the salary-versus-dividend calculus in Ontario, but CPP contribution rates have continued their gradual increase under the CPP enhancement phase-in. That makes it more important than ever to run the numbers before you decide — not after your year-end has already passed.

Don’t Forget the TFSA

Whether you pay yourself salary or dividends, maximizing your TFSA each year is a no-brainer for Ontario small business owners. Investment growth inside a TFSA is completely tax-free, and withdrawals don’t affect income-tested benefits or credits. It works alongside either compensation strategy.

Talk to a CPA Before You Decide

The salary vs. dividend decision touches your personal taxes, your corporate structure, your retirement plan, and your family’s finances all at once. A qualified CPA who understands Ontario’s tax landscape can model both scenarios for your specific situation and help you keep more of what you earn.

Syed CPA Professional Corporation serves small business owners in Milton, Mississauga, Brampton, and across the GTA with practical, plain-language tax and accounting advice. Call Syed CPA at +1 (647) 977-8977 or visit syedcpa.ca to book a consultation.