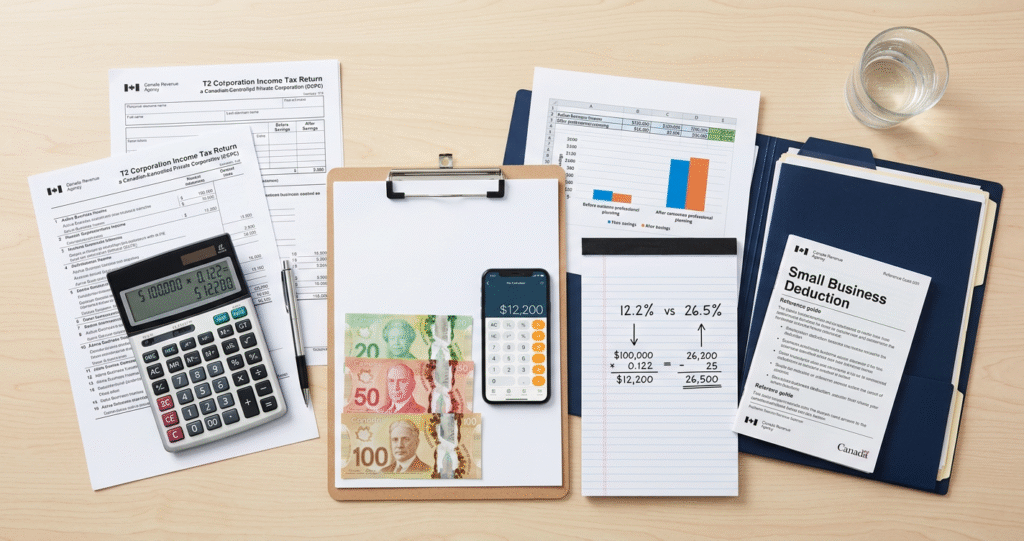

If your business is a Canadian-Controlled Private Corporation (CCPC), you could be paying a combined federal and Ontario corporate tax rate of just 12.2% on your first $500,000 of active business income. That’s a significant break compared to the general corporate rate — but only if your corporation actually qualifies and your accountant is structuring things correctly.

At Syed CPA Professional Corporation, serving clients in Milton, Mississauga, Brampton, and across the GTA, we see many small business owners leaving money on the table simply because they don’t fully understand how the Small Business Deduction (SBD) works — or what can quietly disqualify them from it.

How the 12.2% Rate Works

The combined 12.2% rate breaks down as follows: the federal government applies a 9% tax rate (down from 15% through the federal SBD), and Ontario layers in its own provincial SBD to bring the provincial portion down to 3.2%. Together, that gives eligible CCPCs a blended rate of 12.2% on up to $500,000 of qualifying active business income per year.

Compare that to the general combined rate of roughly 26.5% in Ontario, and you can see why protecting access to the SBD matters so much for your bottom line. On $500,000 of income, that difference translates to roughly $72,000 in tax savings annually.

Common Reasons CCPCs Lose the Small Business Deduction

Not every CCPC automatically gets the full benefit. CRA has built in several reduction and clawback rules that can eat into or completely eliminate your SBD room. Here are the most common triggers to watch for in 2026.

Passive income over $50,000. If your corporation earned more than $50,000 in passive investment income in the prior tax year, your SBD limit starts getting clawed back. It’s eliminated entirely once passive income hits $150,000. If your holding company or operating company is accumulating investment income — from GICs, dividends, or rental properties — this rule can quietly cost you tens of thousands of dollars.

Associated corporations sharing the $500,000 limit. If you control more than one corporation, or if related parties control other corporations, CRA may require those companies to share a single $500,000 business limit. Many business owners with multiple entities don’t realize they’re splitting the pool.

Personal services business rules. If CRA considers your corporation to be a personal services business — essentially, if you’d reasonably be considered an employee of your main client without the corporation — you lose access to the SBD entirely and face higher tax rates on top of denied deductions. This is a growing audit focus area.

Taxable capital exceeding $10 million. For larger CCPCs or those affiliated with larger groups, the SBD phases out as taxable capital climbs above $10 million across associated corporations.

What You Can Do Before Your 2026 Year-End

The good news is that many of these issues are manageable with proactive planning. If your passive income is creeping up, strategies like paying out dividends, investing inside a spousal RRSP, or restructuring how income flows between a holdco and opco can help protect your SBD room. If you have multiple corporations, a formal association review and business limit allocation agreement should be in place before CRA asks the question.

Year-end tax planning for your CCPC isn’t a one-size-fits-all exercise. Salary versus dividend mix, integration with your personal T4 income, CPP contributions as a business owner, and timing of bonuses all interact with the SBD in ways that need to be modeled out — not guessed at.

Talk to a CPA Who Knows Ontario Corporate Tax

If you’re a small business owner in Milton, Mississauga, Brampton, or anywhere in the GTA and you’re not sure whether your corporation is fully benefiting from the Ontario small business deduction, now is the time to find out. A single planning conversation can save far more than it costs.

Call Syed CPA at +1 (647) 977-8977 or visit syedcpa.ca