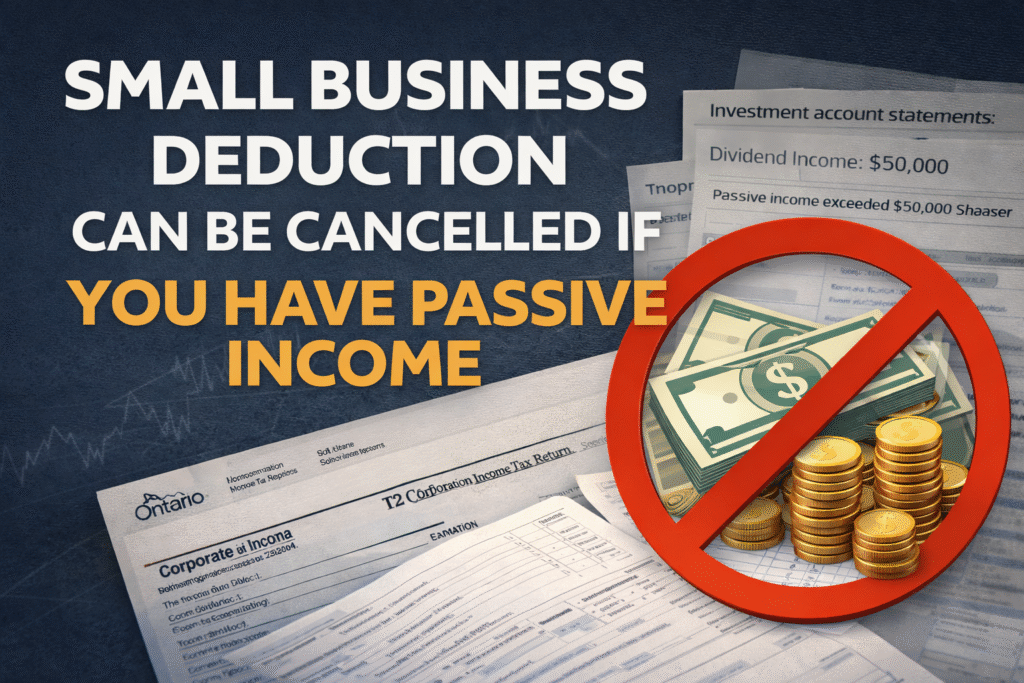

Passive Income Inside Your Corporation: How It Can Quietly Kill Your Small Business Deduction

If you run a Canadian Controlled Private Corporation (CCPC) in Milton, Brampton, Mississauga, or anywhere across the GTA, the small business deduction (SBD) is one of the most valuable tax breaks available to you. It drops your federal corporate tax rate on active business income down to 9% — a significant advantage over the general corporate rate of 15%. But here’s the thing: if your corporation is sitting on investment income, that benefit can quietly start slipping away.

What Is the Small Business Deduction, Exactly?

The SBD lets eligible CCPCs pay a much lower tax rate on the first $500,000 of active business income each year. That $500,000 limit is known as the business limit. For most small business owners, protecting that limit is a core part of their tax strategy. What many don’t realize is that passive income earned inside the corporation can erode — and even eliminate — that limit entirely.

The Passive Income Trap

Starting in 2019, CRA introduced rules that reduce a corporation’s business limit based on its Adjusted Aggregate Investment Income (AAII). If your corporation earns more than $50,000 in passive income in a given year, the SBD starts to phase out. By the time passive income hits $150,000, the small business deduction is completely gone for that year.

The reduction works on a straight-line basis: for every dollar of passive income above $50,000, the business limit is reduced by $5. So at $75,000 in passive income, your business limit drops from $500,000 to $375,000. At $150,000 in passive income, it hits zero. That means your active business income gets taxed at the general corporate rate — and that’s a real cost.

What Counts as Passive Income?

Passive income inside a corporation typically includes interest earned on savings or GICs, dividends from portfolio investments, rental income from property not connected to your active business, and capital gains from investment sales. If your corporation has built up a healthy retained earnings balance and you’ve been parking that cash in investments, this is worth paying attention to.

It’s also worth knowing that capital gains are included at 50% for this calculation — so a large one-time gain in a year can push you over the threshold unexpectedly.

Why This Matters More Than People Think

A lot of Ontario small business owners use their corporation as a savings vehicle — and that makes sense. You’ve already paid low corporate tax on your business income, so leaving money inside the corporation and investing it feels like a smart move. And it often is. But as that investment portfolio grows and generates more passive income, you may unknowingly be clawing back the very tax rate that made keeping money in the corporation attractive in the first place.

The irony is that the more successful your corporation becomes as an investment vehicle, the more pressure it puts on your small business tax rate. It’s a tax trap that sneaks up gradually.

What Can You Do About It?

There’s no single fix, but there are strategies worth considering with your accountant. Some business owners accelerate salary or dividends to reduce retained earnings before year-end. Others look at investing through a holding company structure, using permanent life insurance as an investment vehicle inside the corporation, or shifting some savings into personal accounts like TFSAs and RRSPs where the income doesn’t affect the corporate business limit. Each situation is different, and the right approach depends on your income, your corporate balance sheet, and your long-term goals.

Get Ahead of This Before CRA Does the Math for You

The passive income rules are one of those areas where proactive planning pays off. By the time you’re filing your T2, it’s too late to restructure. If your corporation is generating meaningful investment income, now is the time to review your strategy.

Call Syed CPA at +1 (647) 977-8977 or visit syedcpa.ca